What changes have taken place in people’s income savings and consumption psychology under the influence of the COVID-19 outbreak in Wuhan in early 2020 and the nationwide epidemic rebound mainly in Shanghai in mid-March 2022? What new patterns have emerged in residents’ actual consumption? What are the differences between consumers’ buying behavior in epidemic areas and non-epidemic areas?

In October 2020, December 2021 and April 2022 (during the closure of Shanghai due to the COVID-19 epidemic), Wang Qi, a professor of marketing in China Europe and vice chairman of the Executive Committee of China Europe-Ruian Global Brand Strategy and Fashion Industry Research Fund, led a team to collect nearly 5,000 consumer questionnaires nationwide, and conducted research on issues such as consumers’ income and savings, sustainable consumption, experience consumption and niche hobbies, and new consumption of science and technology.

Since its establishment, the China-Europe-Ryan Global Brand Strategy and Fashion Industry Research Fund has devoted itself to long-term tracking and studying consumers’ consumption psychology, attitude and behavior in each specific economic environment. Since the outbreak of the COVID-19 epidemic in early 2020, the research fund has paid close attention to the changes of consumers’ income, savings and consumption choices in China under the epidemic.

Consumers generally plan to increase savings to cope with the uncertainty of future expectations.

According to the survey data in April 2022, the proportion of people with self-reported personal income increase in epidemic areas was slightly lower than that in non-epidemic areas, accounting for 30.24% and 33.41% respectively, while the proportion of people with personal income decrease was significantly higher than that in non-epidemic areas, accounting for 20.41% and 13.23% respectively. (see the picture below)

Question 1: How did your personal monthly income change in April 2022?

In addition, for different income groups,The population with reduced income in epidemic areas is significantly higher than that in non-epidemic areas.. Whether in epidemic areas or non-epidemic areas, the higher the income, the higher the proportion of income increase, and the lower the income, the higher the proportion of income decrease. Generally speaking,The higher the income, the less the negative impact of the epidemic, and the lower the income, the greater the negative impact of the epidemic.(see the picture below)

Note: Low income means: the monthly income is less than 5,000 yuan; Middle income refers to: monthly income of 5000-10000; High income means: the monthly income is above 10,000 yuan.

Question 2: How did your personal monthly income change in April 2022?

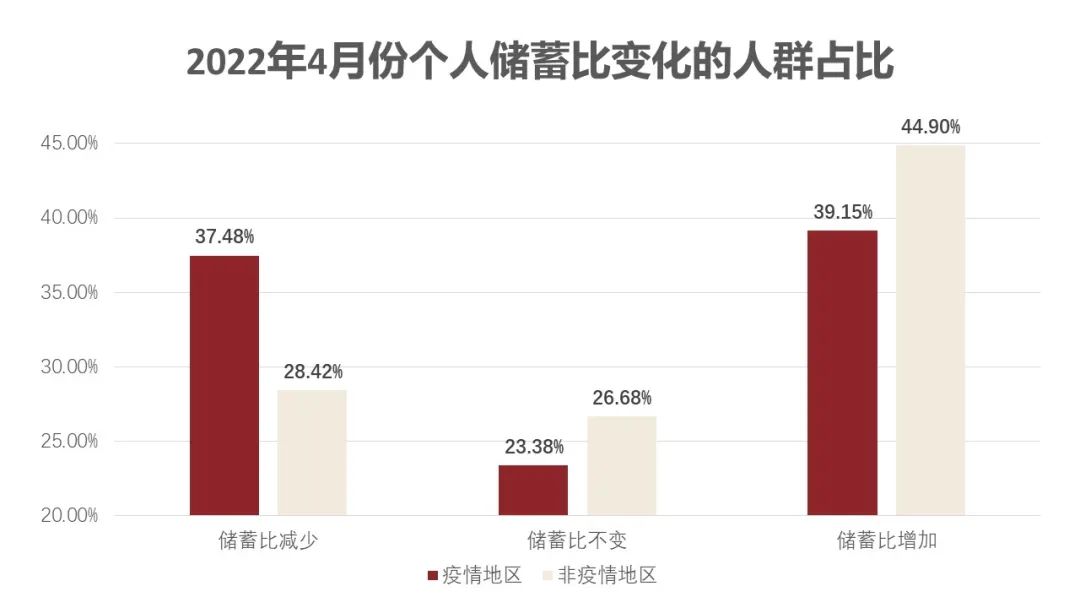

Judging from the savings ratio (the ratio of total savings to total income) in April, the proportion of people with increased savings ratio in epidemic areas is lower than that in non-epidemic areas, while the proportion of people with decreased savings ratio is higher than that in non-epidemic areas, which is not unrelated to the decrease in income in epidemic areas. (see the picture below)

Question 3: In April 2022, what happened to the ratio of your total savings to your total income?

For the savings plan in the third quarter of 2022, nearly 65% of the respondents expect to increase their savings ratio in the third quarter. Compared with non-epidemic areas, this population in epidemic areas accounts for a higher proportion. This reflects that more and more consumers will cope with the uncertainty of future expectations by increasing the savings ratio. just as it is said"If you have money at hand, you don’t panic.". (see the picture below)

Question 4: In the third quarter of 2022, how do you expect to adjust the ratio of personal total savings to total income?

Combined with the survey data after the first outbreak in China, we found that compared with 2020, the personal income situation improved in 2021, and the proportion of people with increased savings ratio also increased greatly, reaching 47.4%. Combined with the income situation, the higher the income, the higher the proportion of people with increased savings ratio. This shows that the consumption desire of all income classes is weakening, especially for high-income people. It can be seen that, in fact, in 2021 (after the first outbreak of the epidemic in China), consumers’ desire for consumption has been greatly weakened. Combined with the data of April this year, it is not difficult to find that this trend is more obvious.How to boost consumer confidence is an urgent problem for the government and enterprises in the second half of the year.(see the picture below)

Question 5: What is the change of your savings ratio (the ratio of total savings to total income)?

The outbreak of COVID-19 epidemic has further widened the income gap among residents, and consumers generally plan to increase the savings ratio to cope with the uncertainty of future expectations.

Although consumers’ income in April was negatively affected by the epidemic to some extent, and the savings ratio is generally expected to increase further, most consumers are still optimistic about the expected income in the third quarter of 2022.Nearly 50% of the respondents expect their income to increase in the third quarter.. (see the picture below)

Question 6: How do you expect your personal monthly income to change in the third quarter of 2022?

Catalyzed by the epidemic containment policy, the "home economy" accelerated its rise.

Residents in epidemic areas are restricted by the policy of closure and control, and the time spent at home has increased significantly.During home life, group buying has become the first choice for everyone’s daily shopping. In the epidemic area, the proportion of people who used group buying in April was as high as 87.57%. Generally speaking, the public’s evaluation of group buying is generally more positive. 81.26% of the people in epidemic areas think that the overall performance of group buying is excellent, which is higher than 75.70% in non-epidemic areas.

According to the survey data in April, 2022, 80% people spend more on food and drink. During the epidemic period, it was difficult to grab vegetables, which made consumers generally choose to increase food and beverage expenditure, and to ease their anxiety and cope with the unexpected situation caused by the epidemic by "hoarding food". In addition to the expenditure on food and drinks, it is also worth paying attention to the purchase of various household appliances that are indispensable for home life. Whether it is the bill of consumers in April or the consumption plan in the third quarter, the proportion of people buying air conditioners, refrigerators, freezers, rice cookers and hot water kettles in epidemic areas is slightly higher than that in non-epidemic areas.As a good cooking helper, the air fryer, which can easily fry everything, is welcomed by consumers in epidemic areas.The proportion of buyers in April was significantly higher than that in non-epidemic areas, reaching 19.29%.

Catalyzed by the epidemic isolation policy,The "home economy" has accelerated its rise. In order to cope with the uncertainty of repeated epidemics in the future, the consumption trend of "home economy" is likely to continue into the third quarter, and consumers tend to make adequate material preparations for home life. (see the picture below)

Question 7: In April 2022, which of the following goods did you buy in the category of household appliances?

Persistence and repetition of epidemic situation,The demand for healthy consumption is soaring.

The persistence and repetition of the epidemic in COVID-19 made the public realize the importance of daily fitness and pay more and more attention to the improvement of physical fitness. During the period of epidemic control, traditional gyms were forced to close down, and online fitness was once sought after by the whole people because of its unique advantages. "Liu Genghong" girls were all over the network. Regarding the choice of fitness methods, our research found that for the fitness methods in the third quarter, people who are willing to choose online fitness are higher than offline fitness in non-epidemic areas; In the epidemic area, a higher proportion of consumers expect to return to the gym after unsealing. (see the picture below)

Question 8: In the third quarter of 2022, which of the following goods do you expect to buy in the category of books/education/fitness/entertainment?

The persistence and repetition of the epidemic in COVID-19 not only make consumers pay more attention to their own health, but also make consumers begin to examine the relationship between human beings and nature and pay more attention to the "environmental protection" of consumption behavior.The green transformation under the hard index of "double carbon" is a big test that many brands and enterprises must deal with.

Through the consumer survey at the end of 2021, we found that "reliable quality" and "having a unified and formal environmental protection label" are the two most important factors to increase consumers’ willingness to buy sustainable fashion products. Therefore, achieving a unified and formal environmental protection label will be an effective means for the government and industry to promote consumers’ willingness to buy sustainable fashion products. For brands and enterprises, we should pay more attention to how to effectively control the quality of the sustainable fashion products they produce, and at the same time increase the quality publicity of relevant products, so as to increase consumers’ confidence in the quality of their products. The survey results show that the primary reason that prevents consumers from buying sustainable fashion products is that they are worried about the unsafe source of product ingredients. For brands and enterprises, how to promote the design of sustainable fashion products is a matter worth thinking about. Publicity design needs to meet consumers’ demand for information on the source of product ingredients, and at the same time, it needs to avoid making consumers have too many negative impressions and concerns.

In addition, about 90% of the respondents bought sustainable fashion products because of their recognition of sustainable concept and expression of sustainable lifestyle, and about 40% of the respondents wanted to gain recognition from society and others. Regarding the price of sustainable fashion products, nearly 50% of the respondents expressed their willingness to pay a premium for sustainable fashion products. About 44% respondents can accept a 10% premium and about 24% respondents can accept a 25% premium for purchasing sustainable fashion products.

From these survey data, we can see that consumers who choose sustainable products are more from the inside. While pursuing environmental protection and sustainability, they are also very willing to pay a certain product premium for sustainability, which means that brands and enterprises can be slightly calm when facing the cost of sustainable transformation. Whether the consumer’s willingness to consume is due to the need of self-health management or the willingness to protect the environment,Brands and products representing healthy lifestyles and concepts will be more likely to be favored by consumers..

Wild camping fever,A new mode of short-distance travel for urbanites

For the consumption plan in the third quarter, the proportion of people who are expected to buy outdoor goods such as ball games, camping tables and chairs, outdoor lights, bicycles, battery cars and skateboards in epidemic areas is higher than that in non-epidemic areas.Outdoor activities represented by camping in the wild have become a new mode of short-distance travel for urbanites.(see the picture below)

Question 9: In the third quarter of 2022, which of the following goods do you expect to buy in the category of outdoor products/transportation tools?

When asked which projects are most likely to be spent in the third quarter, whether in epidemic areas or non-epidemic areas, the top three rankings are: travel (such as go on road trip, group tour, etc.); Outdoor sports (such as surfing, skiing, camping, etc.); Scientific and technological experience activities (AR/VR/MR related immersive experience activities). Although several large cities were seriously affected by the epidemic in the first half of the year, it is not difficult to see that consumers’ desire to travel is still very strong. If major tourist cities can be more comprehensive, accurate and meticulous in epidemic prevention, and provide maximum convenience for tourists on the premise of ensuring epidemic prevention, tourism is still expected to become a hot consumption spot in the third quarter, and together with outdoor sports and technological experience activities, it will become a powerful lever to stimulate the economy.

Camping, as a kind of outdoor activities, its popularity is related to domestic social environment, economic development level, vacation system and the evolution of consumers’ health/nature concepts.

Among them, from the social environment, with the gradual increase of environmental protection in China, there are more and more places with outdoor activities in China.

From the perspective of economic development level, the consumption level of the middle class in China has obviously improved, and to some extent, it has achieved "money and leisure". The improvement of economic level and the popularity of domestic cars have provided a material basis for the popularization of camping as an outdoor activity.

Judging from the vacation system, the paid vacation system in China is still not perfect, which leads to the general concentration of traditional holidays, too crowded travel and poor experience, and instead gives birth to outdoor trips around the country that everyone can take advantage of on weekends.

From the point of view of health, domestic consumers began to look forward to nature more and more, eager to relax the daily pressure of work, which was aggravated by the long-term blockade of the epidemic.

From the perspective of cost, the single economic cost of camping is low, which is also an important reason why camping is more attractive to young people and the middle class than other outdoor sports.

Camping not only provides an excellent scene for friends to contact and parent-child activities, but also meets the sense of life ceremony needed by young people and the middle class.

In addition to outdoor activities can greatly meet the social needs of some consumers, virtual world is also an important way for some consumers to meet their social needs. With the popularity of the concept of "meta-universe" in recent two years, the gradual maturity of related technologies and the upgrading of the demand of pan-entertainment industry, human interest and desire for building a virtual world have reached an unprecedented height. People are not only satisfied with the way of consumption in real life, but more and more consumers are willing to pay for the virtual world. The limited consumption caused by closed control during the epidemic has encouraged consumers’ willingness to spend in the virtual world. Both the endorsement of virtual idols and the immersive experience in virtual games provide consumers with "emotional value" that is difficult to be fully satisfied in real-world social activities. Especially for the young generation in China who grew up in the period of rapid development of mobile Internet, they were born and grew up in a world where reality and virtuality coexist, and they have a strong tendency to buy goods and brands that show "futuristic sense+technology". At the end of 2021, in the survey on whether the brand will affect its purchase intention because of the release of virtual people, more than 70% of the respondents in the youth group (25-34 years old) said that it would increase the possibility of buying the brand products.

tag

The persistent impact of the global COVID-19 epidemic and the rapid iteration of consumption patterns in China market have provided many new opportunities for business development, and various new consumption have emerged, but at the same time, they have also brought many challenges to business practice.

Through the continuous consumption survey in the past three years, on the whole, the public’s awareness of saving is gradually increasing, and the cost is gradually decreasing.To some extent, this means that consumers will pay more and more attention to the cost-effectiveness and practicality of goods when they conduct consumption behavior.In our consumption research in 2020 and 2021, cost performance and practicality have always been the two aspects that consumers think domestic brands perform best. Under the current economic background of tight consumption, this is undoubtedly an excellent opportunity for domestic brands. Whether it is a domestic brand or an international brand, improving the cost performance of its own products will be a necessary condition to attract a wider consumer group.

For the part that consumers are willing to spend, some fundamental changes have taken place in their consumption structure and underlying consumption concept.The long-term home life under the control of epidemic situation made consumers pay attention to the quality of "home life", so the "home economy" was accelerated.Consumers can satisfy their dietary needs by buying various household appliances, so that the quality of life at home can be guaranteed. The persistence and repetition of the epidemic in COVID-19 made people realize the importance of health, so more and more consumers began to choose a healthy and green lifestyle. During the period of epidemic isolation, due to the long-term limitation of physical space, consumers began to be extremely eager to break through the limitation of real space and explore a broader world. They are eager to go to nature and enter the virtual world, expecting to meet their social and emotional needs through these explorations.

At any time, crises always coexist with opportunities. Facing the impact and challenge of the COVID-19 epidemic, there are also great business opportunities in the economic uncertainty and the rapid change of the market. Whether brands and enterprises can take the lead in the crisis and open up new opportunities in the changing situation is the key to determine the parties to stand out in this special economic environment. For the relevant enterprises that meet the current consumption growth trend, what needs to be considered is how to better seize these opportunities, how to further improve the cost performance, quality and design of products, accurately position their own brands, and optimize marketing strategies; For enterprises that are greatly affected by the epidemic, how to adjust their product structure can be considered.Find a profit breakthrough point in meeting consumers’ needs for home, health, outdoor activities and social needs..

(The author is Wang Qi, a professor of marketing at China Europe International Business School)

CBN was authorized to reprint from WeChat WeChat official account "China Europe International Business School".